($TEVA) TL1A paradigm - engineering a Best-in-Class biological

Why a $2.7 billion pipeline asset is still treated as a free call option, while the data points to a $60 intrinsic value.

Introduction

At the core of the current bullish thesis for Teva is duvakitug (TEV-48574), a human IgG1 monoclonal antibody targeting the tumor necrosis factor-like cytokine 1A (TL1A). To understand the clinical significance of the recent data, one must first appreciate the precision engineering behind the molecule.

TL1A is a pro-inflammatory cytokine that binds to the DR3 receptor to amplify immune signals and mediate fibrosis—the scarring of intestinal tissue that often leads to surgery in IBD patients. However, the body also possesses a “decoy” receptor, DcR3, which naturally neutralizes excess TL1A to maintain homeostasis.

Unlike first-generation competitors, duvakitug was specifically selected for its ability to block the pro-inflammatory TL1A-DR3 signaling while retaining binding to the DcR3 decoy receptor. This dual-action approach—inhibiting the “gas pedal” of inflammation while leaving the “brakes” intact—theoretically offers a more nuanced regulation of the immune response, potentially leading to the superior efficacy observed in the RELIEVE trials.

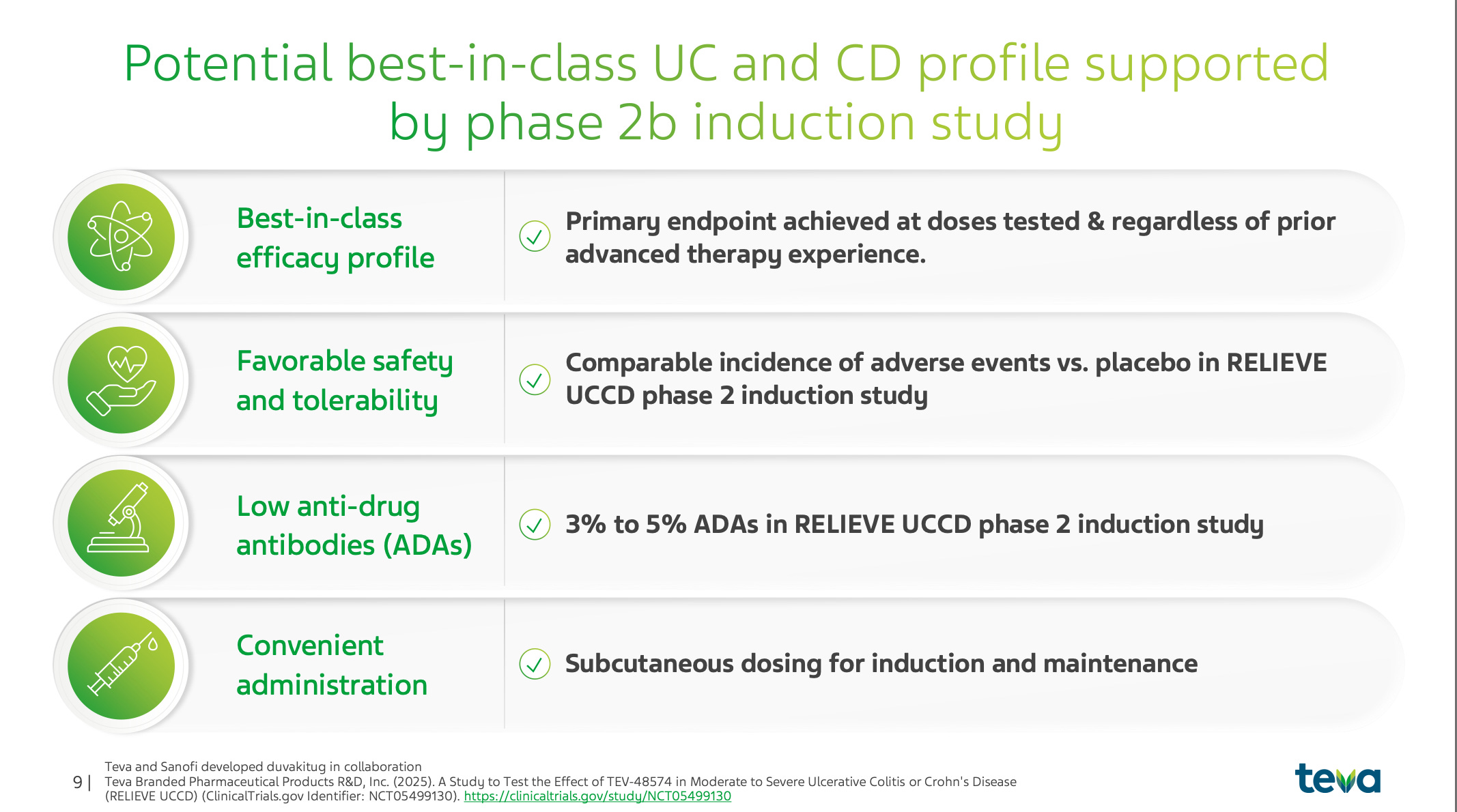

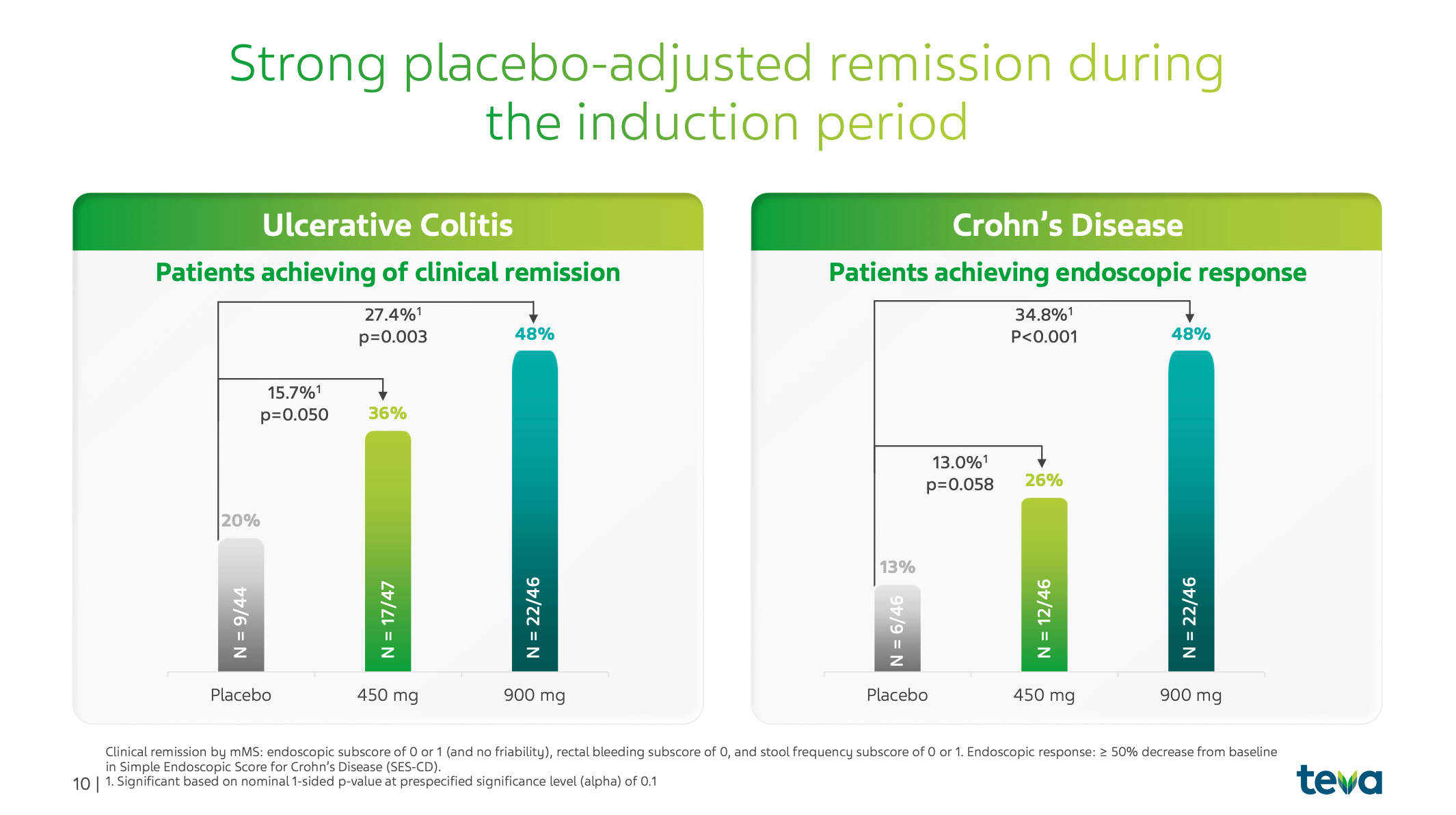

Phase 2b Maintenance Data

Let us break down the results across the two primary indications: Ulcerative Colitis (UC) and Crohn’s Disease (CD).

1. Ulcerative Colitis (UC) - Sustaining deep remission

In the 44-week maintenance portion of the study, which enrolled patients who had successfully achieved a clinical response during the 14-week induction phase, duvakitug demonstrated remarkable durability.

900 mg Dose: 58% of patients achieved the primary endpoint of clinical remission.

450 mg Dose: 47% of patients achieved clinical remission.

The significance here lies in the absolute responder rates. When compared to historical Phase 2 data from other TL1A competitors like tulisokibart (32-48% remission) and afimkibart (34-36% remission), duvakitug’s 58% rate sits at the top of the class.

2. Crohn’s Disease (CD) - Addressing the fibrotic challenge

Crohn’s Disease is often considered a higher-unmet-need market due to the high frequency of surgical intervention (up to 75% of patients). Duvakitug’s maintenance data in CD focused on endoscopic response, a more rigorous objective measure than symptomatic reporting.

900 mg Dose: 55% of patients achieved an endoscopic response.

450 mg Dose: 41% of patients achieved an endoscopic response.

These results are particularly impressive given that the maintenance period utilized Q4W (every four week) dosing, a reduction from the Q2W dosing used in the induction phase. This suggests that duvakitug possesses the potency and half-life required for convenient, monthly subcutaneous administration without sacrificing efficacy.

Competitive Landscape

Cross-trial comparison

While cross-trial comparisons require caution, the trend is undeniable. Duvakitug has consistently shown the highest absolute clinical remission rates in UC and endoscopic response rates in CD among its TL1a peers. Even when compared against established Phase 3 biologics in other classes (such as IL-23 inhibitors like risankizumab or JAK inhibitors like upadacitinib), duvakitug’s placebo-adjusted induction rates suggest it could become the preferred first-line advanced therapy.

Safety and immunogenicity

A “best-in-class” title requires more than just efficacy; it requires a pristine safety profile. In the RELIEVE studies, duvakitug showed a comparable incidence of adverse events to placebo. Crucially, the rate of Anti-Drug Antibodies was exceptionally low, ranging from 3% to 5%. Low immunogenicity is a critical factor for long-term “maintenance” therapies, as it reduces the risk of the patient’s immune system neutralizing the drug over time.

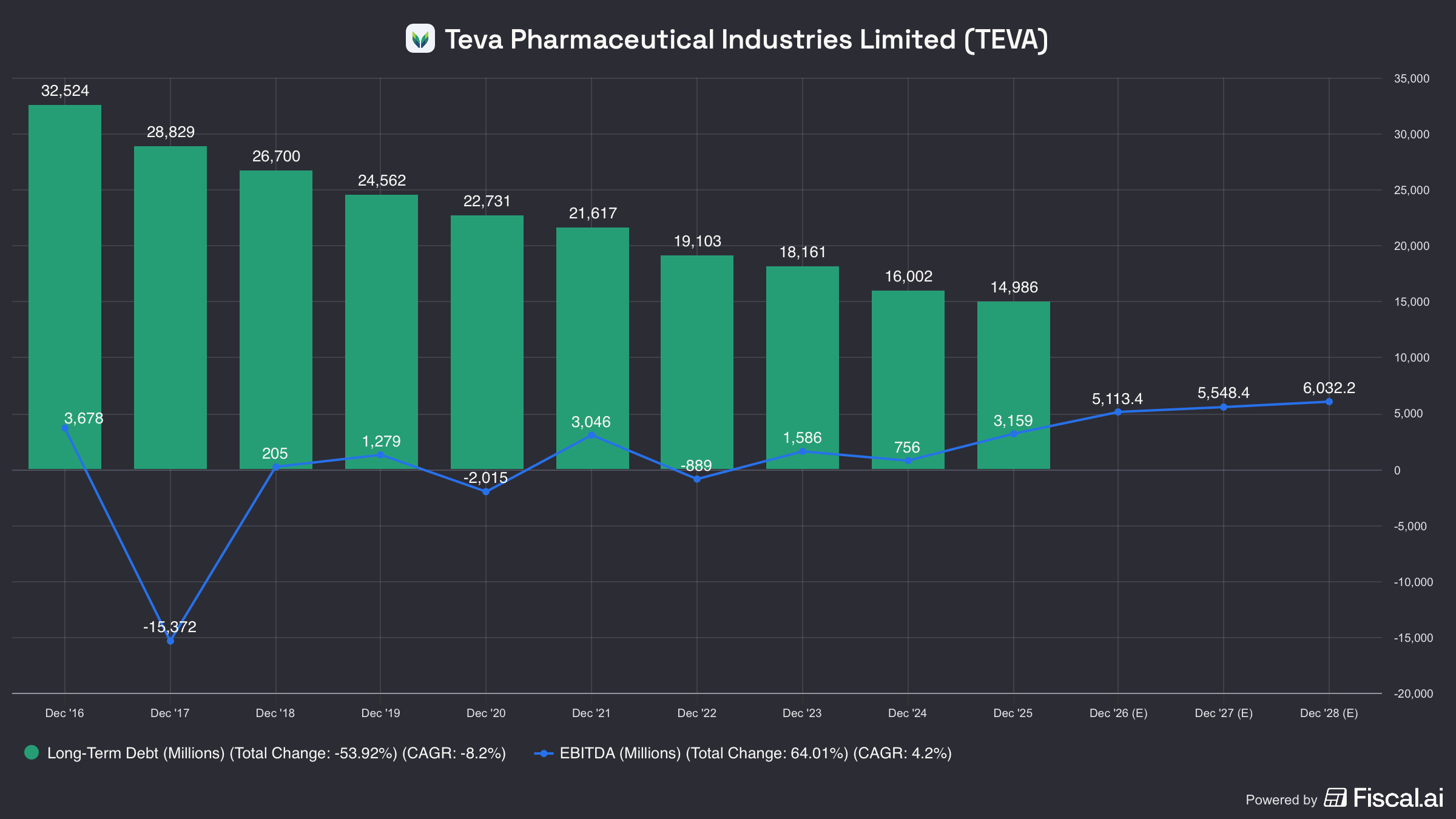

The primary “bear” argument against Teva historically has been its debt pile. However, the logic of the “Pivot to Growth” strategy is now being validated by clinical data.

Revenue generation: Branded assets like Austedo are now generating the cash flow ($2.2B+ in 2025) necessary to fund these high-stakes Phase 3 trials.

Risk sharing: The 50/50 profit and R&D cost-sharing agreement with Sanofi meaningfully de-risks the capital-intensive Phase 3 program. Teva received $250M milestones for both CD and UC Phase 3 initiations in Q4 2025 alone.

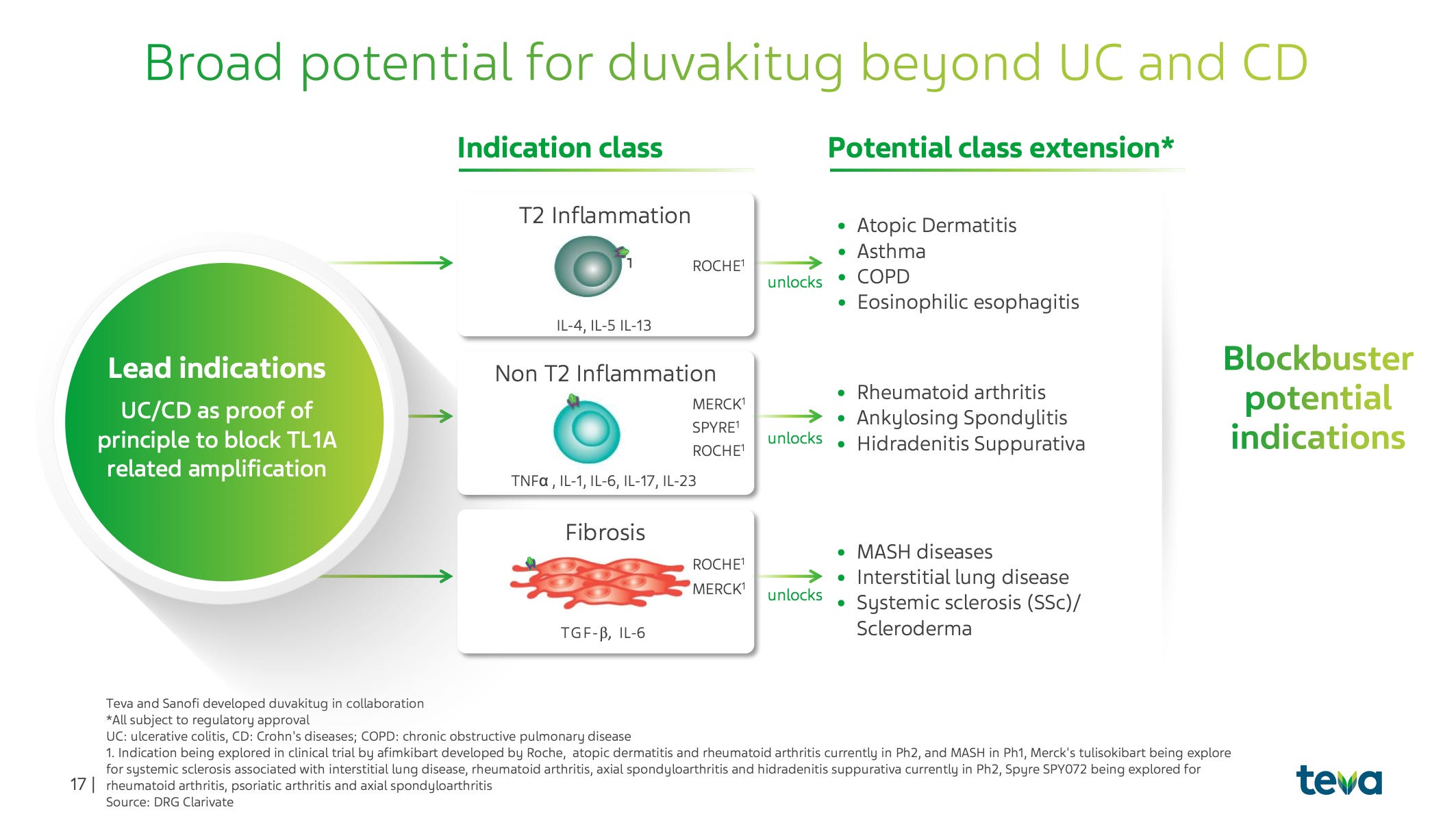

Pipeline breadth: Duvakitug is being positioned as a “pipeline in a molecule”. Beyond IBD, TL1A signaling is implicated in Atopic Dermatitis, Asthma, and Fibrosis. Teva plans to disclose additional indications in the second half of 2026, which could significantly expand the TAM. This feels similar to another very popular drug class.

And just a quick reminder of the debt reduction:

Valuation implications

The release of the maintenance data provides a “fundamental floor” for Teva’s stock price. When looking at the valuation implications, several factors suggest a significant re-rating is imminent.

Peak sales potential

The consensus for duvakitug peak sales in UC and CD has hovered around $2.0B. However, given the best-in-class data and the “all-comers” approach (which maximizes the patient pool by not requiring specific biomarkers), peak sales models of $2.7B to $5.0B are plausible.

Valuation multiples

Historically, Teva has traded as a troubled generic company at roughly 6-7x forward earnings. This is a massive discount compared to “slow growth” pharma like Pfizer (~12x) or high-growth innovators like Eli Lilly (30-50x).

The transition to a branded biopharma innovator justifies a valuation re-rate. I have previously stated that I see $58-60 USD in three years time. A DCF that supports a $58–60 Teva share price in three years assumes that management delivers on its pivot: revenues grow from roughly flat in 2026 to mid‑single‑digit growth thereafter, operating margins step up toward ~30% by 2027 as cost savings and product mix kick in, and net debt/EBITDA falls toward ~2×, letting more EBIT drop through to EPS and FCF. On those assumptions, EPS can rise from about $3.3 in 2025 to roughly $5.0–5.5 by 2028, with free cash flow per share around $4.0–4.5 . Discounting these cash flows at ~9% with a 2% terminal growth rate yields a terminal EV/FCF multiple of about 13–14×, which corresponds to an 11–12× P/E on 2028 earnings and an intrinsic value in the high‑$50s to $60 range.

Conclusion and outlook

The Phase 2b maintenance data for duvakitug is not just a “good result”; it is a competitive victory, Eric Huges referred to it at the call as “Best-in-Disease”. By showing 58% clinical remission in UC and 55% endoscopic response in CD, Teva has produced the most potent TL1A data to date.

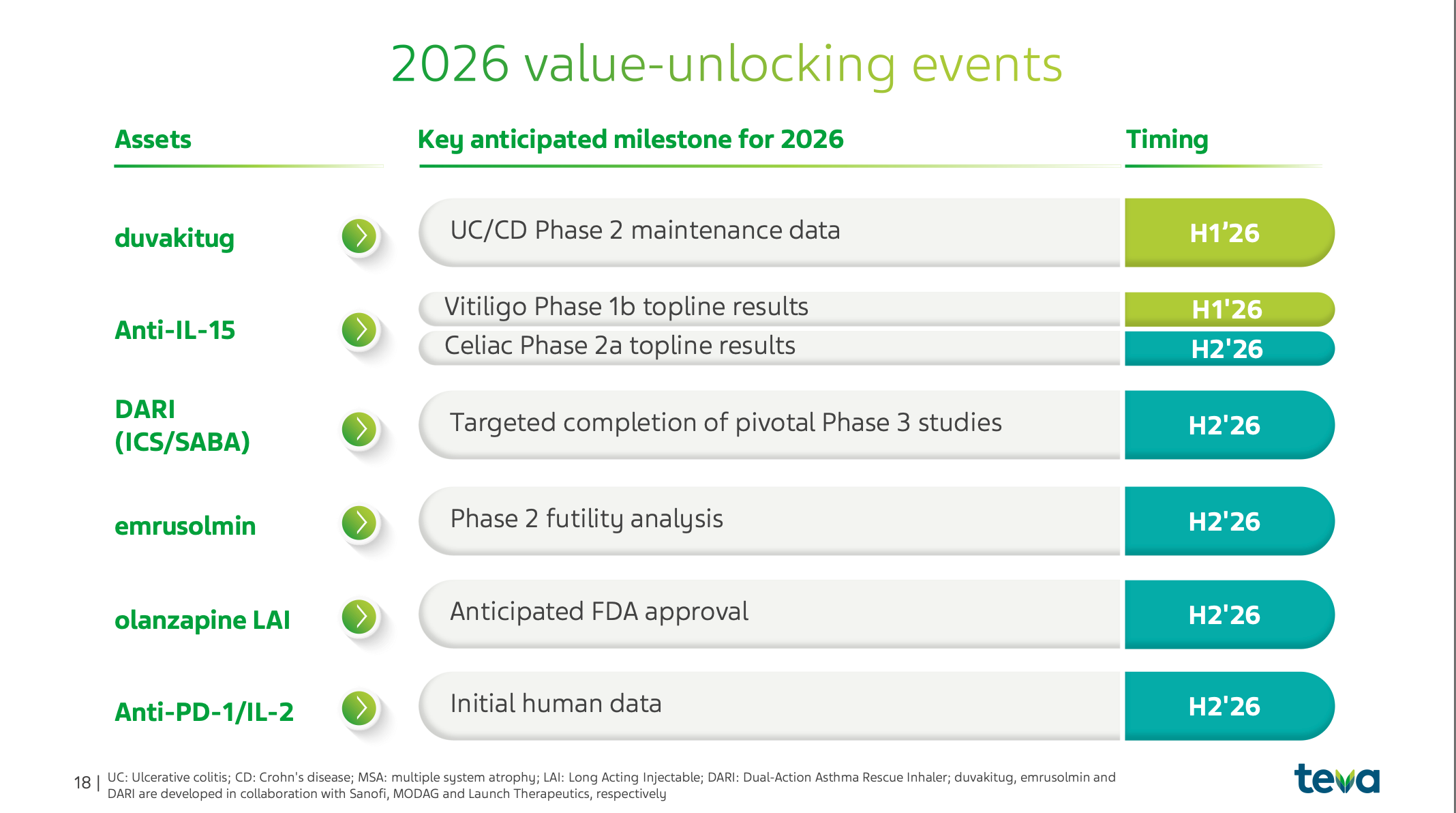

The scientific rationale, blocking DR3 while retaining DcR3, appears to be translating into superior clinical outcomes. With Phase 3 studies already underway and a plethora of other catalysts coming in 2026 (including olanzapine LAI approval and data for Anti-IL-15 in Vitiligo), the narrative for Teva has officially shifted from “stabilization” to “acceleration”.

The duvakitug maintenance data de-risks Teva’s most valuable pipeline asset, confirming its potential as a best-in-class therapy. Combined with aggressive debt paydown and a portfolio of growing branded assets, the company is fundamentally undervalued.

The results provide more optimism about the future for Teva and I believe we will see share price of $58-60 in 24-36 months.

I have a position in Teva, the above is as always not investment advice.

With that, thanks for reading I truly appreciate the interest. Below are a few ideas for further readings and inspirations.