EssilorLuxottica ($EL.PA): Blending Vision, Technology, and Compounding in Eyewear

Looking Sharp — Literally and Financially

Introduction

EssilorLuxottica (EL) represents a unique investment opportunity at the crossroads of healthcare, fashion, and technology. As the world's largest vertically integrated eyewear company, EL benefits from a wide economic moat rooted in brand strength, distribution control, and manufacturing efficiency. With a structurally growing market—driven by aging populations, emerging middle-class consumers, and increasing awareness of eye health—the company is well positioned to compound value over the long term. However, investors must assess the current valuation, which appears elevated at a forward P/E of 35x for 2025.

Business Overview

Formed in 2018 by the merger of French optical lens leader Essilor and Italian eyewear frame and retail powerhouse Luxottica, EL now controls more than 15% of the global eyewear market. The company operates across the full value chain, from innovation and design to manufacturing and retail, allowing it to capture margin at every stage. It owns iconic brands such as Ray-Ban and Oakley and holds exclusive licensing agreements with luxury fashion houses including Prada and Chanel. Its network includes around 18,000 retail stores globally (13,500 corporate stores and 4,100 franchise stores) and extensive e-commerce platforms.

In 2024, EL generated €26.5 billion in revenue, up 6% in constant exchange rates. Operating profit reached €4.4 billion, with a margin of 16.7%. Net income was €3.1 billion, supported by robust growth in all key regions and product segments.

The company is a quality compounder.

Segment and geographic performance

EL divides its business into two core segments: Professional Solutions (wholesale) and Direct-to-Consumer (retail). In 2024, DTC accounted for 55% of revenue and saw double-digit growth in Q4, led by strong online sales and store-level performance from banners such as LensCrafters and Sunglass Hut.

North America, EL’s largest market (45% of revenue), accelerated to 7.8% growth in Q4, supported by strong uptake of Ray-Ban Meta smartglasses and a resilient lens business. Europe, Middle East & Africa (EMEA) grew 9.6%, buoyed by new product rollouts and optical subscriptions. Asia-Pacific surged 14%, driven by China's 50%+ growth in Stellest myopia control lenses. Latin America returned to growth with strong performance in Colombia and Brazil.

Meta collaboration: Smart-glasses as a strategic catalyst

The 2023 launch of Ray-Ban Meta, in partnership with Meta Platforms, marks a major strategic move into wearable technology. These smartglasses integrate audio, video, and AI features into the classic Ray-Ban design, providing a form factor with mass-market appeal. Over 2 million units have been sold since launch. U.S. customers represent about two-thirds of all sales. EL has sold 3,700 Ray-Ban Meta per day since launch, and for (some) comparison, Apple sold 20,000 units per day of the original iPhone. Apple now sells about 602,740 iPhones per day.

Smart-glasses now account for approximately 75% of EL’s Q4 growth in North America. Despite seasonal sales peaks around the holidays, EL has successfully positioned Ray-Ban Meta as more than a gimmick. With Meta’s AI assistant, livestreaming capabilities, and integrated microphones and cameras, EL has carved a niche in wearable tech where many have failed.

Competitively, Ray-Ban Meta stands apart from offerings like Snap Spectacles, which lacked fashion credibility, and Bose Frames, which lacked full connectivity and app ecosystem support. Apple has long been rumored to enter AR eyewear but has yet to bring a product to market. EL’s first-mover advantage, style authority, and manufacturing scale offer a unique edge, though broader consumer adoption will hinge on price points, battery life, and evolving user habits.

Financial analysis and valuation

EL is a cash-generative business with strong growth visibility. Revenue is forecast to grow at a CAGR of 6% through 2029, reaching over €36 billion. EBIT margins are expected to expand from 16.7% to nearly 20%, driven by vertical integration, manufacturing efficiencies, and improved inventory management.

EPS is projected to grow from €6.81 in 2024 to €11.21 by 2029. Free cash flow was €2.4 billion in 2024, after €1.5 billion in capex, reflecting consistent reinvestment into store network modernization, R&D, and direct-to-consumer infrastructure.

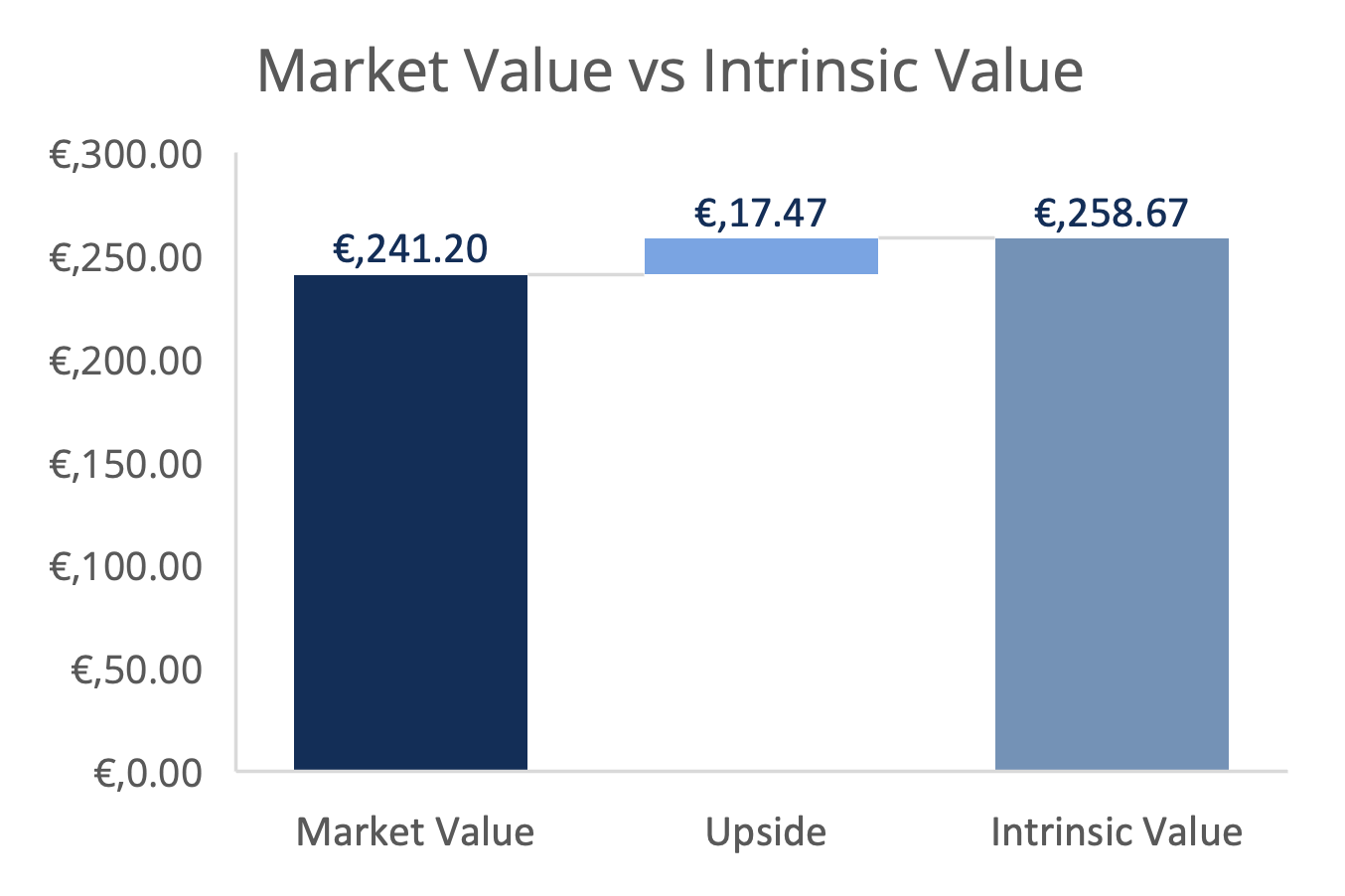

Here is what I get from the DCF model:

Valuation multiples are demanding. At a share price of €241:

Forward P/E (2025): 31.2x

EV/EBITDA: 16.5x

Price/Book: 2.7x

Dividend Yield: 1.68%

Equity Free Cash Flow Yield: 2.8%

While these multiples imply some margin of safety, EL’s valuation reflects its leadership, growth optionality, and strategic execution. Comparing PEG (Price-to-Earnings-to-Growth), the ~2.8x ratio (31.2x P/E vs. 11% EPS CAGR) remains above historical levels but is in the range of quality compounders.

Moat and competitive advantage

EL enjoys a strong moat anchored in brands, patents, retail presence and cost advantages through scale, automation, vertical integration. Ray-Ban and Oakley are top global eyewear brands with very high consumer awareness. Its distribution network gives luxury brand licensors unmatched reach, enabling partnerships with Prada, Versace, and others.

The lens business adds a quasi-monopoly dynamic. EL controls over 40% of global optical lens volume, with a research budget that accounts for 75% of the entire industry. The company holds over 11,000 patents in lens technology and chemical coatings. Its Stellest lens for myopia control and Nuance Audio for mild hearing loss represent meaningful optionality in med-tech.

Top 10 eyeglass lens manufacturers, including their country of origin, specialty areas, and strengths:

M&A strategy and vertical integration

EssilorLuxottica has long followed a strategic approach of consolidating the fragmented eyewear industry. The landmark merger that created the company is core to its desire to control all stages of the value chain. Post-merger, EL has continued to acquire local optical retail chains across geographies to gain distribution access and reduce dependence on third-party sellers.

Vertical integration has been a source of both margin improvement and competitive strengthening. EL designs and manufactures its own lenses and frames, distributes them through its wholesale and owned channels, and controls pricing and customer experience via retail and e-commerce. The strategy enables the company to upsell innovation and ensure high gross margins even in competitive environments. Acquisitions like GrandVision and more recent smaller players in Asia and Latin America reflect a consistent pattern of geographic and channel expansion.

Nuance Audio: Expanding the Med-Tech frontier

In parallel with Stellest and Ray-Ban Meta, EL is advancing its Nuance Audio initiative. Designed for individuals with mild hearing loss, Nuance Audio products integrate discreet audio amplification into everyday eyewear, blending form and function.

Cleared in the U.S. for OTC distribution and launching in select European markets, Nuance aims to address the massive unmet need among aging consumers who are hesitant to adopt traditional hearing aids. The product leverages EL’s retail network to drive accessibility, and its appeal lies in its familiar (glasses), stylish presentation.

While still early in commercialization, Nuance could become a meaningful long-term driver, tapping into the hearing care market currently dominated by specialized players. If successful, Nuance Audio could represent the convergence of vision, hearing, and lifestyle needs—opening an entirely new segment for the company.

Sustainability and strategic initiatives

EL has aligned its sustainability strategy with business growth. It was recently included in the Dow Jones Europe Index and “Fortune’s Change the World” list. More than 40% of new collections are made with sustainable materials, and the company is engaging consumers in in-store circularity programs.

It also collaborates with the World Health Organization’s SPECS 2030 initiative and has facilitated access to vision care for nearly 1 billion people since 2013, with over 33,000 rural optical points globally.

Risks to monitor

Despite its strengths, there are always risks that needs monitoring:

Tariffs & Supply Chain: Smartglasses are exclusively manufactured in China. Any disruption could materially impact EBIT.

Insurance exposure: Approximately 60% of revenue at LensCrafters is funded by insurance plans. U.S. healthcare policy changes could affect accessibility.

Currency sensitivity: EL's cost base is EUR-heavy while significant revenue is in USD.

Retail exposure: The company’s vast physical store base provides control, but also increases fixed costs and vulnerability to footfall decline, especially in the sunglasses category.

Innovation pressure: R&D-heavy products like Stellest and Nuance Audio have long adoption cycles. Commercial success is not guaranteed.

Industry context and competitive landscape

The global eyewear industry is growing at 3-4% annually, supported by aging demographics, increasing screen time, and expanding access to eye care. Yet the market remains fragmented, especially in lenses and optical retail, where independent providers still dominate.

Competitors include The Cooper Companies (specialty lenses), Johnson & Johnson Vision, and Hoya. However, none offer the same vertical integration and brand power. New entrants in wearable tech (e.g., Apple, Snap) pose potential disruption, especially if fashion and utility converge in AR.

EL’s key strategic response has been to integrate tech in aesthetically accepted formats, like Ray-Ban Meta. If successful, it can out-maneuver tech rivals lacking style credibility and scale manufacturing.

Conclusion

EssilorLuxottica’s blend of healthcare fundamentals, fashion branding, and smart technology positions it as a one-of-a-kind global player. While its shares trade at a premium, its market leadership, innovation capability, and solid financials make it a viable long-term holding.

The Meta partnership adds excitement and optionality, though it is still early days there is a possible real-time AI growth horizon in play as well - although regulatory aspects in especially Europe can dampen this. Provided EL can navigate macro risks and maintain its brand relevance, it remains a compounder with defensive traits and high-quality growth.

I do not have a position in EssilorLuxottica but have it on my watchlist and find the company to be high quality. The above is however not intended as investment advice.

With that, thanks for reading I truly appreciate the interest. Below are a few ideas for further readings and inspirations.