Nike ($NKE) Benched: This one stay on the sidelines

Introduction

Nike has long been heralded as the titan in the athletic apparel and footwear market, boasting one of the most beloved brands that has transcended generations and geographical boundaries. Yet, beneath the surface, cracks have begun to form prompting me to dive deeper into what is happening. I adopt a cautious and somewhat bearish stance towards Nike, driven by concerns about weakening fundamentals, intensifying competitive dynamics, and strategic missteps that may take considerable time to rectify. With this article I want to present a balanced yet critical perspective, highlighting the underlying risks that investors should be mindful of as they assess Nike’s future prospects.

Nike’s current situation and strategic reset

Nike’s latest earnings report for the third quarter of fiscal 2025 has done little to inspire confidence. The company reported revenues declining 9% year-over-year, driven by pronounced softness in key markets, notably Greater China. While a mild sales beat slightly mitigated initial expectations, a deeper examination reveals more substantial challenges. Greater China, a market critical to Nike’s growth narrative, saw revenues plunge 17%, marking its third annual decline in four years. The persistence of these challenges underscores Nike’s ongoing struggle to regain footing amid geopolitical, competitive, and internal operational headwinds.

Moreover, Nike’s previous pivot toward lifestyle and fashion segments now appears overly ambitious, exacerbating the inventory buildup of unsold lifestyle products. The management’s new strategic roadmap involves aggressively liquidating excess inventory, repositioning digital channels, and re-emphasizing athletic performance products. These corrective actions are necessary (athletic performance branding is what has build the brand), but involves risks: significant upfront costs, continued margin pressure, and an uncertain timeline for tangible improvements.

The recently appointed CEO Elliott Hill is implementing the “Win Now” strategy—focusing on innovation, wholesale partnerships, and revitalized marketing — seems like all the right levers, but will not yield results short term. Nike’s challenges, particularly in China and digital distribution, are deep-rooted and unlikely to dissipate swiftly.

A strategic deep dive: Challenges and Response

Nike’s strategy today centers on three core areas: product innovation, channel restructuring, and regional market recovery, particularly in China.

Product innovation & marketing efforts

Historically, Nike distinguished itself with cutting-edge innovation, exemplified by technologies such as AirMax and ZoomX cushioning. However, the past several years have seen relative stagnation. Nike’s historical dominance in performance footwear —particularly running — has eroded with the rise of competitors like Hoka and On, who have stolen significant market share with fresh designs and strong consumer resonance.

Nike is now investing heavily to regain momentum, enhancing its product pipeline with renewed R&D spending exceeding $500 million annually. While these investments are vital, regaining lost market position will likely require prolonged and sustained execution. High promotional activities and margin erosion reflect Nike’s near-term struggle to maintain premium pricing power amidst an inventory surplus.

Channel and Inventory Management

Over recent years, Nike aggressively pushed into direct-to-consumer (DTC) sales, simultaneously reducing dependence on wholesale channels. Though intended to elevate margins and brand control, this pivot unintentionally alienated many wholesale partners, creating friction in key retail relationships. Today, Nike finds itself backtracking, re-engaging with select wholesale partners to manage excess inventory and re-establish broader consumer touchpoints.

Moreover, inventory mismanagement remains a major pain point. Nike has resorted to drastic markdowns, creating near-term margin pressure. While inventory clearance is essential, investors must recognize the consequent margin compression, which will likely persist until at least late fiscal 2026.

Greater China: A lingering concern

China, once Nike’s fastest-growing market, is now its Achilles’ heel. Sales growth has reversed dramatically amid rising nationalism, local competition from brands like Anta and Li Ning, and geopolitical frictions affecting consumer sentiment. Regaining lost ground won’t be easy.

Nike is attempting to restore growth through localized marketing initiatives, tailored product innovation, and expansion of flagship stores. Yet, these efforts require significant upfront investment without guaranteed short-term returns. Nike’s path back to sustainable growth in China remains uncertain.

In Europe, there might also be more headwinds building as European consumers are currently more conscious about whom they purchase from, and are looking to shift spend away from American companies to European ones. For now this is more anecdotal than hard facts, but it is a movement that currently has momentum.

Financial Analysis:

Revenue and EPS trajectory

Nike’s projected revenue growth paints a sobering picture. Fiscal 2025 revenue is expected to decline by approximately 10% year-over-year, with continued declines of around 2% anticipated in fiscal 2026. Only by fiscal 2027 is a modest recovery of around 4% projected. The sluggish rebound trajectory raises concerns about whether Nike can quickly recover market share, particularly in key lifestyle and running categories.

EPS forecasts align with this cautious outlook. Nike’s adjusted EPS peaked at $3.73 in fiscal 2024 but is anticipated to plummet to $2.13 in fiscal 2025, then dip further to $1.90 in fiscal 2026 before partially recovering to $2.65 in fiscal 2027. The slow and uncertain pace of earnings recovery contrasts sharply with more optimistic expectations priced into current valuation levels, suggesting ongoing downside risk. We will come back to the ongoing downside.

Margin compression and profitability

Nike’s EBIT margins have come under substantial pressure. From a peak EBIT margin of 14.3% in fiscal 2022, margins have shrunk significantly to an expected 7.6% in fiscal 2025. The main drivers are rising promotional activities, inventory markdowns, and sustained investments in marketing and innovation—required to reinvigorate the brand but detrimental to short-term profitability. Recovery in EBIT margins to historical levels of mid-teens seems unlikely in the next few years, given current sales and inventory dynamics.

Return on Invested Capital (ROIC), historically a Nike strength, further underscores concerns. ROIC is projected to decline from a robust 52.6% in fiscal 2024 to 29.6% in fiscal 2025, then further to 26.1% in fiscal 2026. This drop highlights deteriorating efficiency in utilizing capital to generate returns—again reflective of Nike’s operational and strategic missteps.

Valuation: Persistent downside risks

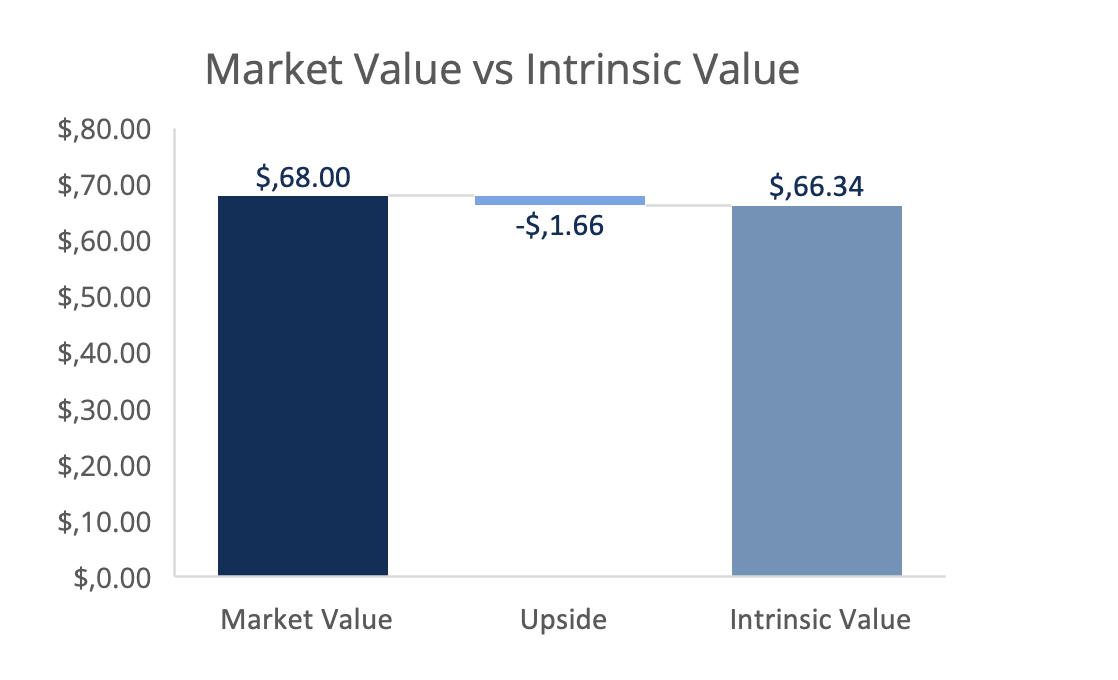

Nike currently trades at approximately $68 per share, reflecting a mid-30s P/E multiple— significantly above its historical average of roughly 24x. This elevated multiple signals market optimism for a rapid, “V-shaped” earnings recovery. Yet, underlying business challenges suggest a far slower, potentially “L-shaped,” earnings trajectory. If market expectations recalibrate to reflect this slower recovery, a substantial P/E compression toward historical averages could occur, presenting meaningful downside risks.

Employing a conservative forward earnings multiple of 25x on fiscal 2027 projected EPS of $2.65 yields a price target of roughly $66, indicating downside risk from current levels. Discounted Cash Flow (DCF) modeling supports this valuation, with intrinsic value estimates closely aligning around $66 per share, reinforcing that current price levels may still underestimate medium-term headwinds.

From the model:

Technical view

In the words of Paul Tudor Jones: “Nothing good happens below the 200-day moving average”

Nike’s technical outlook remains decidedly bearish, highlighted by the stock trading significantly below its downward-sloping 200-day moving average, which currently stands roughly around $85-$90. The persistent negative gap between Nike’s price and its 200 DMA underscores sustained selling pressure and bearish investor sentiment, indicating that the stock remains entrenched in bear-market territory. Additionally, Nike’s recent breakdown below critical support around $68 on increased volume, coupled with bearish momentum signals from indicators like the MACD, reinforces concerns of further downside potential. Although short-term oversold conditions could trigger temporary rebounds, substantial resistance from the 200 DMA suggests any rally might quickly face selling pressures, confirming caution for investors considering positions at current levels.

Competitive landscape: A threatening backdrop

Competitors pose another significant risk to Nike’s turnaround narrative. In addition to formidable global rivals like Adidas and Lululemon, fast-growing brands like On and Hoka have rapidly captured consumer attention in running segments—a crucial category historically dominated by Nike. Simultaneously, native Chinese brands have increasingly leveraged nationalistic sentiment, presenting a tangible risk to Nike’s aspirations in its critical Chinese market.

As Nike attempts a strategic pivot back to performance products, these competitors —many with leaner operations and lower promotional burdens—continue gaining share. Competitive pressures will likely prolong Nike’s margin struggles and may necessitate higher promotional expenditures to regain lost market share.

Conclusion: A loooong game

Nike undeniably possesses powerful brand equity, substantial scale, and financial resources to eventually right its ship. Yet, current strategic misalignments, margin erosion, competitive threats, and sluggish turnaround timelines all warrant a cautious stance. Investors should remain wary of valuations predicated on overly optimistic rebound scenarios and recognize that a meaningful EPS recovery and margin stabilization may take several years.

While Nike remains fundamentally sound enough to avoid a severe long-term structural decline, the road ahead looks difficult and extended. Given current valuation multiples, persistent downside risks, and uncertain timeline for recovery, I maintain a cautiously bearish view on Nike shares at current levels.

I have no position in Nike but keep it on my watchlist. The above is also not intended as investment advice.

With that, thanks for reading I truly appreciate the interest. Below are a few ideas for further readings and inspirations.

IOn my end I remain bullish on Nike specifically long term. As strategic investment I do not see the brand losing over the next decade, even if this means a couple of years of bumping road due to past bad decisions. The new approach that resembles the real Nike can pay. Super interesting and well written as always 🫡🔥

Nice article man!