Update on Teva

Continues to look bright, potential for accelerated debt reduction.

Teva Pharmaceuticals is anticipated to experience significant upside potential beyond short-term fluctuations. UBS and Argus recently adjusted their targets for Teva. Here we will go into what that means and how Teva is expected to perform.

Key factors influencing this outlook include potential API sale proceeds, positive data from the TL1a Ph2 study, and strong FY24 financial performance. The stock has faced a recent decline, but the outlook remains positive for the second half of 2024.

Key Catalysts for 2H24

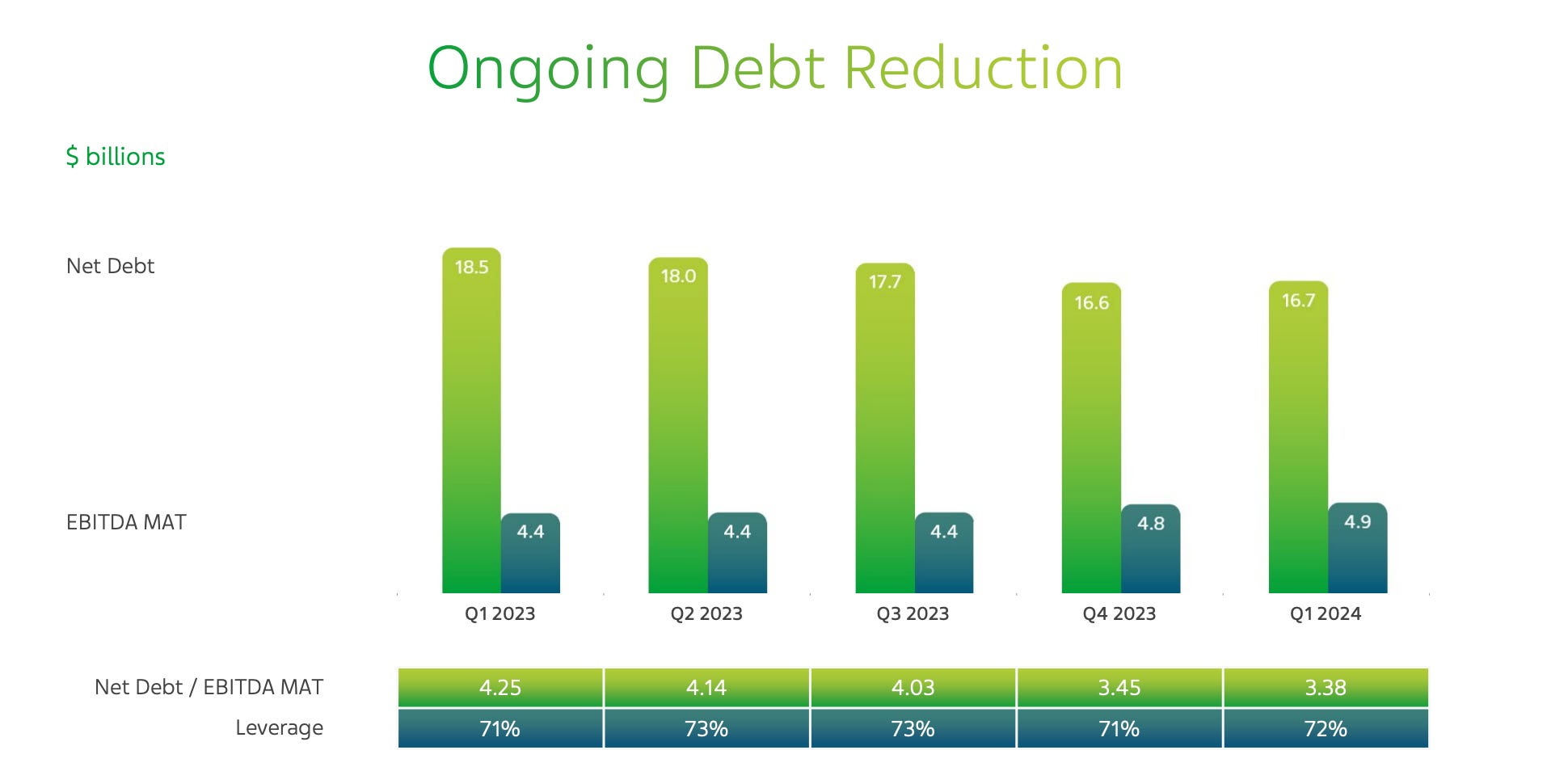

1. API Sale Proceeds: Expected proceeds from an API sale could range between $4.8 billion and $6.8 billion, which would enable quicker deleveraging. This would be very positive for Teva, and would dramatically accelerate the ongoing debt reduction. If a sale ends up in the middle of the expected range, Teva could bring down debt to around 2.5x EBITDA.

2. TL1a Ph2 Data: The Phase 2 study for TL1a, likely to yield positive results based on prior validations, is anticipated to be a significant catalyst.

3. FY24 Financial Performance: Potential for Teva to exceed guidance, with 2024 sales/EBITDA estimates at $16.2 billion/$4.9 billion, higher than consensus estimates of $16.0 billion/$4.8 billion.

2Q24 Financial Preview

Sales and Earnings: Sales are expected to reach $4.1 billion, due to robust performance in Austedo and US generics. EBITDA and EPS estimates have been trimmed to $1.18 billion and $0.57, respectively, due to a lower gross margin profile.

Austedo: Q2 sales forecast increased to $401 million, driven by strong quarterly performance.

Generics: US generic sales for Q2 are projected to be $920 million, benefiting from g-Revlimid sales.

Gross Margin: Revised down to 52.8%, reflecting company commentary from the Q1 call.

Long-term Outlook and Valuation

Price Target Increase: The price target has been raised to $24 from $22, driven by an expected increase in EBITDA multiple for the mature business.

Litigation Risks: Potential legal liabilities include settlements related to Copaxone kick-backs, generic price fixing, and Copaxone Europe antitrust issues, with an estimated total liability of $2.2 billion.

Valuation Method: The valuation is based on a Sum-of-the-Parts (SOTP) analysis, considering both branded and mature products, with respective multiples applied to forecasted sales and EBITDA.

For more recent take aways on Teva, read the summary from the Goldman Sachs Healthcare Conference.

Market Performance and Risks

Recent Stock Performance: Teva's stock had decreased by approximately 10% over the past three weeks due to various short-term issues but bounced back after UBS revised its target upwards.

Key Risks: Include the failure of clinical trials for TL1a and Olanzapine LAI, slower-than-expected adoption of Uzedy, and Austedo sales not meeting expectations.

Quantitative Assessment

Industry and Regulatory Environment: Expected to improve over the next six months.

Earnings Surprise Potential: Likely to see a positive earnings surprise relative to consensus expectations due to better-than-expected base business performance.

Upcoming Catalysts: The next significant catalyst is the earnings report expected around July 31, 2024.

For a summary of Teva´s first quarter results, read more here:

This sentiment and analysis reflects an optimistic outlook for Teva, with key drivers being strategic sales, robust product performance, and potential positive clinical trial outcomes. The valuation has been adjusted upwards in light of these factors, despite some manageable legal and market risks.