Riding the AI Wave: How NVIDIA’s Financial Strength is Shaping the Future

Analysis of NVIDIA’s Quarter and Future Outlook

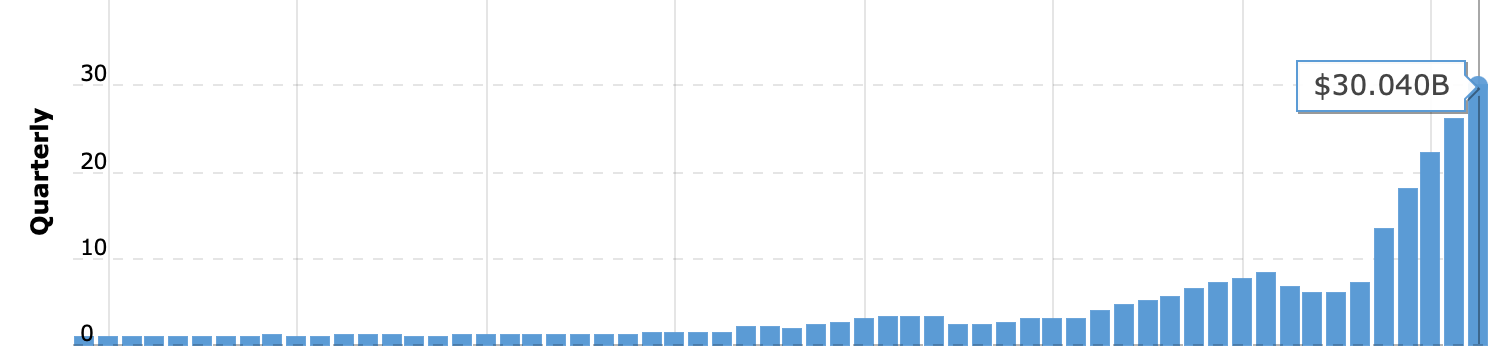

NVIDIA’s recent quarterly performance offers a comprehensive look into the financial health and strategic direction of the company, especially as it continues to dominate the AI hardware market. For the most recent fiscal quarter, NVIDIA reported revenues of $30.04 billion, slightly exceeding the market’s expectations of $29.93 billion. This marks a staggering 122.4% year-over-year growth, driven primarily by the explosive demand for its data center products, which continue to serve as the backbone for AI development across various industries.

NVIDIA quarterly revenue development:

One of the standout aspects of NVIDIA’s quarterly results is the company’s gross margin, which came in at 75.7%, slightly above the guidance of 75.5%. This robust margin reflects NVIDIA’s ability to maintain pricing power in the highly competitive AI hardware market, as well as its efficiency in scaling production to meet surging demand. Operating margins also remained strong at 66.4%, a slight improvement from the previous quarter, further emphasizing NVIDIA’s operational efficiency.

NVIDIA’s data center segment was particularly impressive, generating $26.3 billion in revenue—a 154.5% year-over-year increase. This growth was fueled by the adoption of NVIDIA’s GPUs in AI applications, where their performance advantages are crucial for large-scale data processing and machine learning tasks. The continued roll-out of products like the H100 Tensor Core GPUs and the forthcoming Blackwell series is expected to sustain this growth trajectory.

For the upcoming quarter, NVIDIA has provided revenue guidance of $32.5 billion, with gross margins expected to slightly dip to 75%. This conservative guidance reflects a degree of caution, likely due to the anticipated initial lower margins from the launch of new products like Blackwell. However, the company’s management has stated that margins should normalize as production scales and cost efficiencies are realized.

Looking further ahead, NVIDIA is projecting revenues of $127.7 billion for the full fiscal year, with expectations of maintaining strong operating margins around 66.5%. The company’s outlook is underpinned by continued demand from cloud service providers (CSPs) and sovereign customers, who are increasingly investing in AI infrastructure. Notably, the sovereign customer segment is expected to grow to represent nearly 10% of NVIDIA’s total revenue, driven by large-scale AI investments by governments worldwide.

The Growing Role of AI-Accelerated Compute Hardware in IT Budgets

As the adoption of artificial intelligence (AI) continues to expand, organizations across industries are increasingly recognizing the critical need to invest in AI-accelerated compute hardware. This shift is reflected in the spending patterns of Chief Information Officers (CIOs), who are beginning to allocate a significant portion of their IT budgets towards this burgeoning technology. According to recent survey data, CIOs currently spend approximately 5% of their IT budgets on AI-accelerated compute hardware. However, this figure is expected to rise dramatically, with a compound annual growth rate (CAGR) in the mid-40% range, reaching nearly 15% of IT budgets over the next three years.

The Strategic Shift Towards AI Investment

This anticipated increase in spending on AI hardware is driven by several factors, including the growing demand for more powerful computing capabilities to support the development and deployment of AI-driven applications. As AI technologies become more sophisticated, the computational power required to train and operate these systems also increases, necessitating significant investments in specialized hardware.

Moreover, the rapid advancements in generative AI (GenAI) are prompting organizations to re-evaluate their IT priorities. As companies work to formulate their GenAI roadmaps, many are finding it necessary to reallocate resources from other projects to support their AI initiatives. Notably, 33% of CIOs are defunding other projects, with legacy systems and infrastructure upgrades being the most affected. This reallocation reflects a broader trend of organizations prioritizing AI as a key driver of future growth and competitiveness.

The Implications for Legacy Systems and Infrastructure

The defunding of legacy systems and infrastructure projects highlights the challenges organizations face in balancing the need to maintain existing systems while also investing in new technologies. For many companies, the shift towards AI represents a strategic pivot that requires difficult decisions about where to allocate resources.

However, it is important to note that a majority of CIOs are not defunding other projects to finance their AI investments. This suggests that while AI is a priority, it is being funded through incremental investments rather than by diverting resources from other areas. This approach allows organizations to pursue AI initiatives without compromising the stability and functionality of their existing IT infrastructure.

The Economic Impact of AI Hardware Investment

The economic implications of this trend are significant. The expected mid-40s CAGR in AI hardware spending indicates that enterprises are increasingly willing to allocate substantial portions of their budgets to this area.

This willingness to invest heavily in AI hardware is likely to have far-reaching effects on the broader technology landscape. Companies that specialize in AI hardware, such as NVIDIA, are poised to benefit from this surge in demand. NVIDIA’s recent performance, demonstrates the company’s strong position in the AI hardware market. The report highlights NVIDIA’s significant growth in data center revenues, driven by the increasing adoption of its AI-accelerated hardware solutions.

A Strategic Imperative

The shift towards AI-accelerated compute hardware is not just a trend; it is a strategic imperative for organizations looking to remain competitive in the digital age. As CIOs continue to increase their investments in AI, the technology’s role in shaping the future of business will only grow. This trend underscores the importance of forward-thinking IT strategies that prioritize AI while balancing the needs of legacy systems and infrastructure.

Valuation and Conclusion

From a valuation perspective, NVIDIA remains an attractive investment, especially given its dominant position in the AI hardware market. The company’s stock is currently trading at a price-to-earnings (P/E) ratio of approximately 25.8x based on projected earnings for the upcoming fiscal year. While this might seem high compared to traditional semiconductor companies, it is justified by NVIDIA’s unparalleled growth prospects and the high barriers to entry in the AI hardware market.

NVIDIA’s consensus price target seems to be around $150 per share, reflecting good confidence in its ability to maintain its leadership in the AI space. This valuation is supported by NVIDIA’s robust financial performance, its strategic product roadmap, and its ability to capitalize on the rapidly growing demand for AI-accelerated compute hardware. The company’s forward-looking strategies, including the scaling of Blackwell GPU production and the expansion into sovereign AI projects, are likely to drive continued revenue growth and margin stability.

NVIDIA’s financial performance and future outlook highlight its strong position in the AI-driven future of technology. With significant investments from enterprises and governments alike as well as new innovation frontiers like AI and biology, NVIDIA is poised to capture a substantial share of the growing AI hardware market. The expected increase in CIOs’ IT budgets dedicated to AI, alongside NVIDIA’s strategic initiatives, positions the company as a key enabler of the AI revolution. As such, NVIDIA remains a compelling investment for those looking to capitalize on the transformative potential of AI.

Finally, let´s have a look at some of the numbers from the model:

As always, there is lots of uncertainties and arguably NVIDIA is entering into a period now where the incremental gains in share price is going to get more and more difficult, so bear that in mind. Still, NVIDIA is firmly one of the largest companies in the world with innovation power like few companies that have ever existed. If things go well we will see significant EPS expansion supported by world class cash generation.

That is it for now, thanks for reading along, much appreciated.

Further readings:

Interesting, specially form the valuation and future growth perspective. Anyhow, what potential challenges do you think could impact its ability to maintain its dominant position in the market, especially considering the fast pace of technological advancement & competition?